BYD dominates Chinese EV market in October

19 December 2023

In a record month for China’s electric vehicle (EV) registrations, domestic brand BYD ruled the best-seller charts. José Pontes, data director at EV-volumes.com, analyses the market.

China saw more than 808,000 EVs registered in October, making it the third month of record battery-electric vehicle (BEV) and plug-in hybrid (PHEV) deliveries in a row. With the country’s zero-emission market on an upward trajectory, the last two months of the year can also be expected to produce best-ever results.

This means China represented 60% of global EV registrations in October, with four plug-in models leading the country’s overall passenger car market in the month. This serves to highlight the country’s progression as a leading EV market, backed by several domestic manufacturers and a public that is ready to adopt the technology.

Looking at market share, EVs accounted for 39% of all deliveries in October, with BEVs alone making up 26% of registrations. The EV share across the first 10 months of the year hit 36%, with 24% for BEVs. Considering the current growth rate, plug-in models could end the year with close to a 40% share of the Chinese automotive market.

BYD boom in October

BYD took the top five places in the best-selling EV chart in October, with only two foreign models making it to the top 20.

The BYD Song was on top once again, with its BEV and PHEV registrations amounting to a record total of 63,965 units. Of this, 10,982 were all-electric, another best for the model. However, while the Song has dominated the Chinese EV market in 2023, competition is mounting, especially from its sibling models.

Second was the BYD Yuan Plus, with another best-ever monthly performance seeing 40,019 units delivered. The vehicle leads China’s compact category at a time when a price war is causing strong competition. This means the Yuan Plus is becoming less profitable for BYD, as it aims to maintain its position above contenders such as the GAC Aion Y.

The BYD Qin Plus reached 38,273 registrations to place third, with the BEV version alone scoring 9,383 deliveries. With prices starting at CN¥100,000 (€12,787), demand is strong despite internal BEV competition from the BYD Seal. Meanwhile, the BYD Destroyer 05 poses a threat to the PHEV option.

Yet the lower price point should mean the Qin Plus can continue to post impressive results at the expense of its pricier siblings. In the midsize category, the model has almost twice the number of registrations as the second-place GAV Aion S and should easily take the category crown for the year.

BYD’s dominance in the October market continued in fourth place with the Seagull, which recorded 37,836 registrations in the month. The model is expected to be a star player for the brand as it continues to ramp up deliveries. The Seagull could win a best-seller title in 2024, but it is overseas where the vehicle may prove disruptive.

Latin America and Africa are waiting for an appealing, budget EV that can push the technology into the mainstream. The Seagull could also make BYD a leading brand in places like India and Europe, where good, small, value-for-money BEVs are scarce.

Sitting somewhere between the A and B-segments with a purposeful angular design, it profits from the brand’s blade batteries, in 30kWh and 39kWh sizes. While the more affordable Wuling Bingo came eighth, it only features a 17kWh battery and no DC charging.

Rounding out BYD’s top-five domination in October was the Dolphin, posting 28,353 registrations. BYD seems focused on sending units to export markets, content with around 25,000–30,000 units per month in its domestic market. This should still allow the model to make regular appearances in China’s top five.

Record results for carmakers

Just over a thousand units separated fifth and sixth place, with the GAC Aion Y achieving a best-ever 26,132 deliveries. The model could break into the top five soon, disturbing the BYD and Tesla duopoly that has ruled the Chinese market for several months.

However, Tesla did not have a strong month in October. The Model Y came seventh with 23,353 registrations, while the Model 3 did not make the top 20. With the refreshed version of the D-segment EV now available and the carmaker’s quarterly delivery schedule, it should bounce back into the charts later this year.

The Wuling Bingo managed 23,744 deliveries on its way to eighth, while Li Auto saw all three of its models record their best performance. The L7 ended October in 12th with 15,525 registrations, while the L9 scored its third strongest-ever monthly performance in a row with 12,756 deliveries putting it in 14th. Just below came the L8 with 12,142 units.

The smaller Changan Lumin (15,533 units) and Geely Panda Mini (13,052 units) also hit record sales, slotting them into 11th and 13th respectively. Elsewhere, the Volkswagen (VW) ID.3 posted a record 11,812 registrations putting it in 16th. As the price war in China continues, the model’s lower price point should help sales.

Outside the top 20, the Chinese EV market highlighted its diversity. In the startup category, XPeng’s G6 scored 8,741 registrations, continuing its climb up the chart. The new model should join the top 20 soon, possibly as early as December, as its production ramp-up continues.

Leapmotor’s T03 had its best result since June 2022 with 6,381 registrations, while the C11 stayed at near-record levels with 8,769 registrations. FAW saw its Hongqi E-QM5 end the month in 21st with 10,021 registrations, just 42 units short of joining the top rankings.

Meanwhile, Geely enjoyed good news across its long list of brands. The Zeekr 001 recorded a solid 8,517 registrations, while in their third month on the market, the Lynk & Co 08 PHEV and Galaxy L6 achieved 8,039 and 4,374 registrations respectively.

A sub-brand of SGMW, Baojun’s new compact MPV, the Yunduo, also improved, hitting a record 5,439 registrations in October. Meanwhile, Great Wall’s investment in PHEVs paid off, with a few models having a record month. The Haval Raptor PHEV hit 5,084 registrations, and the Tank 500 PHEV scored 5,065 registrations. With the Tank 400 PHEV landing in October and taking an already significant 3,102 units, this side of Great Wall can be expected to start posting some serious figures.

From foreign OEMs, the VW ID.4 posted 7,209 registrations, a new best this year for the German crossover. The BMW i3 was another foreign model rising up the ranks. With 5,763 registrations, the midsize EV is helping the brand recover some traction in the plug-in market.

Song stretches its lead

Looking at the results across the first 10 months of the year, the BYD Song is well above its competition with 492,201. Meanwhile, the second-place BYD Qin Plus kept the Tesla Model Y at bay. With just 23,991 units separating the two, and Tesla looking towards a strong December, there is the potential for a change in the last two months of the year.

In fourth, the BYD Dolphin was surpassed by its stablemate, the Yuan Plus. There is also potential for another inter-carmaker swap to occur in sixth, through GAC’s leading models. The Aion S currently sits above the Aion Y, however the former lost significant ground to its crossover sibling in October, with only 3,276 units between the two.

Another model on the rise is the BYD Seagull. Despite not moving from 10th, it recovered significant ground on the BYD Han in ninth and should surpass it in November. The little BYD could even reach sixth by the end of December.

In the second half of the table, the Wuling Bingo keeps rising, having jumped three positions in October to 11th.

Meanwhile, all three Li Auto models are now in the top 20, with only BYD having more representation in the year-to-date chart. The L7 should also climb to 15th in November, as it sits very close behind the Denza D9.

Finally, the last position change in the table happened in 19th, with the Geely Panda Mini surpassing the BYD Destroyer 05.

BYD dominates the brands

In the brand rankings, there was no big position change in October. BYD held 35% of the market and is looking to win its 10th EV carmaker title this year. Meanwhile, Tesla’s grip grew weaker, ending the month with 7.5%, down from 8.1% in September. The brand is stable in second place.

Third-place GAC Aion surprisingly lost share in October, taking 6.4% of the market, compared to 6.6% in the previous month. This was due to the slowdown in registrations of the Aion S. SGMW witnessed improved performance, taking 5.6% of the market, up from 5.4%.

In fifth, Li Auto kept growing, taking a 4.6% share, up from 4.5% in September. Behind, Changan in sixth (4.3%, up from 4.2%) and Geely in seventh (4%, up from 3.8% in September) are looking to return to the best-seller table.

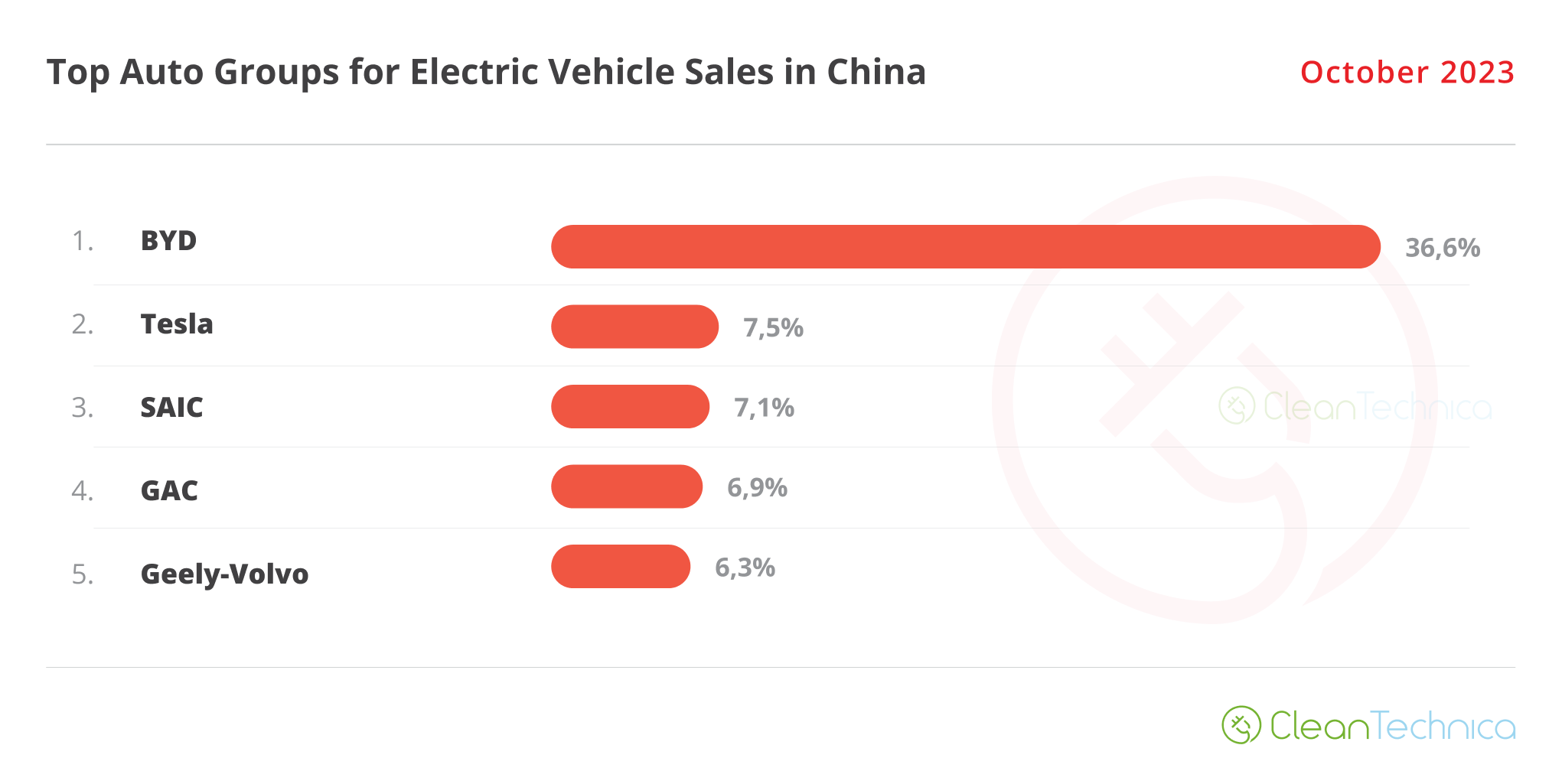

Looking at automotive groups, with brands brought together under their parent company umbrellas, BYD leads comfortably. Holding a 36.6% market share, it dropped slightly from 36.7% in September.

Tesla remains firm in second (7.5% share), but SAIC is closing in on the US carmaker with 7.1% of the market, profiting from SGMW’s good results. Fourth-place GAC is also nearby with a 6.9% share, down from 7.1% in September.

One step down, fifth-place Geely–Volvo grew, now at 6.4% share, up from 5.9% in the previous month. Below it, Changan in sixth (4.8%, up from 4.6% in September) gained some precious ground over Li Auto (4.6%) in seventh. Yet the gap between the two is small, and a position change could occur in November.

{kind=link}