Insight: EVs to remain niche proposition, despite solid growth prospects

14 March 2018

14 March 2018

Sales of electric vehicles (EVs) across the Big 5 European markets grew by 50% in 2017 on the back of new model launches and consumer concerns about the impact of diesel cars on the environment. According to data from EVVolumes.com, sales of battery electric vehicles (BEVs) topped 87,500 units, while those of plug-in hybrid electric vehicles (PHEV) were slightly lower at 76,527. However, research by Autovista Group suggests that even with the current dynamic development of the EV sector, EVs will remain niche until well into the next decade.

Combined BEVs and PHEVs accounted for just over 1.5% of all vehicles sold in France, Germany and the UK last year. However, with sales of just over 5,000 units, EVs made up just 0.25% of all new car registrations in Italy. In Spain, EVs took a 0.6% share of registrations.

Despite significant investment in charging infrastructure, which resulted in an 80% increase in the number of charging locations across Italy in 2017, and the launch of several new PHEV models, including the BMW 2 Series Active Tourer and Mercedes GLC 350e, take-up of EVs in Italy still languishes behind that in its European neighbours. EVVolumes.com puts this down to FCA being relatively slow of the mark in terms of EV development. Fiat enjoys a strong following in its national market, which typically translates to higher sales and residual values at home; in the short term, this strength of following appears to be shaping EV demand.

Growth in Italy is expected to strengthen in 2018, as the German PHEVs establish themselves on the market and further investment in infrastructure makes owning an EV more practical. However, at 65%, growth is still expected to lag behind Germany where sales of PHEVs are predicted to double and those of BEVs to rise by 80%. The rate of market expansion will be slowest in France and the UK despite the positive influence from recent relaunches, such as the new generation Renault Zoë and Nissan Leaf and the imposition of a ban on heavily polluting vehicles – particularly diesels – in major cities. Sales in France are expected to increase by 31% to reach just under 56,000 vehicles; in the UK, the growth of 33% this year will take the market up to just under 66,000 units.

EVVolumes.com predicts that 2% of new cars sold in the Big 5 European markets this year will be EVs. The strong growth anticipated in Germany will mean that almost 3% of cars sold there will be electric. In Italy, EVs will still account for less than 0.5% of new car sales.

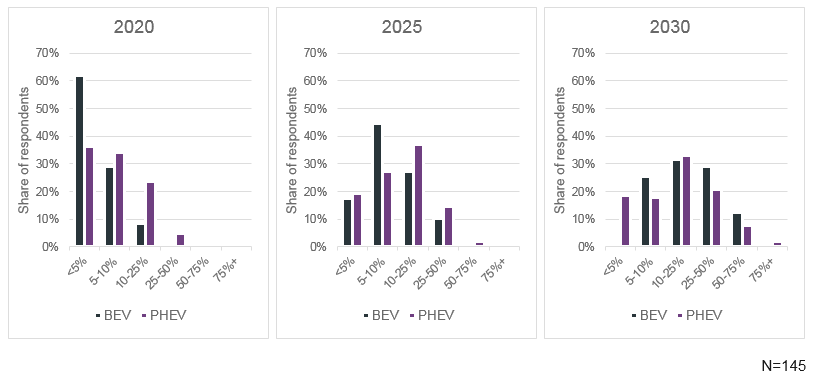

EVs are likely to remain a niche sector in the short term. Almost two-thirds of automotive executives think that by the end of the current decade, BEVs will still account for less than 5% of the car parc; PHEVs are likely to occupy a higher share, but will still account for less than 10% of vehicles on the road.

To understand the outlook for EVs over the next 30 years, Autovista Group asked automotive executives working within vehicle manufacturing, leasing and financing what proportion of the car parc would be powered by an alternative powertrain by the end of the decade and then five, ten years and 30 years after that date. This reveals a gradual shift from the current situation where there are relatively few BEVs to a scenario in 2050 where, according to 20% of respondents, BEVs accounted for more than three-quarters of the vehicles on the road. A further 20% thought that by the middle of the century, BEVs would make up between 50-75% of the car parc.

However, the proportion of PHEVs is not expected to change as significantly, suggesting that as the technology develops battery electric will become the dominant powertrain and hybrid models will begin to fall by the wayside. According to one-third of respondents, PHEVs would still account for less than 5% of cars on the road; a further one-third thought the proportion of PHEVs would sit somewhere between 5-10%. Five years later in 2030, one-third thought PHEVs market share would be in the region of 10-25% – a picture that was repeated in predictions for 2030 and 2050.

Purchasing incentives are critical for short to mid-term development of the consumer sector. Over a quarter of executives felt this was the most important factor currently driving market demand; around half of survey respondents listed this among the three most important factors stimulating market demand. In most of the Big 5 markets, current incentive schemes will steer consumers towards BEVs, EVVolumes.com has suggested; in France, the difference between the subsidies for PHEVs and BEVs is relatively small, meaning that the Bonus-Malus scheme is likely to bolster demand for both vehicle types relatively evenly.

Price is another critical issue for consumers. Some 23% of respondents to the Autovista Group survey felt that parity of acquisition and running costs between EVs and tradition powertrains was the top factor that will boost EV demand among consumers, putting it a close second behind incentives.

When it comes to fleets, emissions regulation was the most important factor shaping demand, followed closely by interest from user-choosers about EVs. However, half of respondents felt that EVs were simply not suitable for business. Limited range and slow charging rates meant that fleet managers were not confident that an EV would be ready and available for use whenever a company car driver needed one or could reliably get them to their destination wherever that happened to be.

BEVs and PHEVs as a percentage of the future car parc in 2020, 2025 and 2030