12 March 2018

After years of phenomenal sales growth in the EU5, more than one in every four cars sold is an SUV. This performance has outpaced growth in the wider new car market but demand broadly outstrips supply in the used car market. As a result, residual values for SUVs are at higher levels than for cars in all other segments in the EU5. But what happens next? As supply to the used car market increases and buyers drift away from diesel – the dominant fuel type for SUVs – have SUV residual values peaked?

Residual value performance

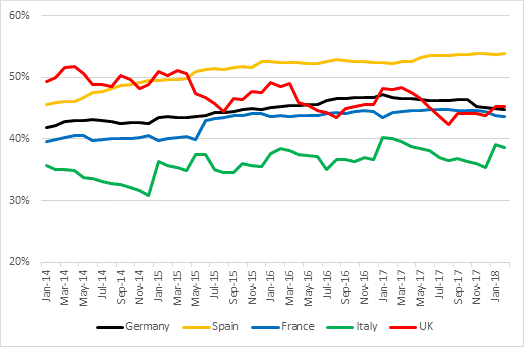

The high level of demand for SUVs has translated into strong residual values across the EU5, with SUVs depreciating less than cars in the wider market in each case. The latest valuations for SUVs, measured as a percentage of list price after 36 months and 90,000km, are between 3-6 pp (percentage points) above the national average in all five markets.

With the exception of the UK, residual values for SUVs are also higher in all markets than they were at the beginning of 2014. This is most pronounced in Spain, where average residual values for SUVs in February 2018 were 8pp higher than they were at the start of 2014. Values are 3-4 pp higher in France, Germany and Italy but 4pp lower in the UK.

RV percentage trends for SUVs in the EU5, 36 months/90,000km, Jan 2014 – Feb 2018

However, the gap between values of SUVs in the EU5 and the respective national average has not changed significantly over the period since 2014. The UK is the exception to this rule as the gap has even narrowed from 11pp early in 2014 to just 5pp according to Autovista Group data for February 2018. In fact, the gap has narrowed so much that it is now less than in Germany.

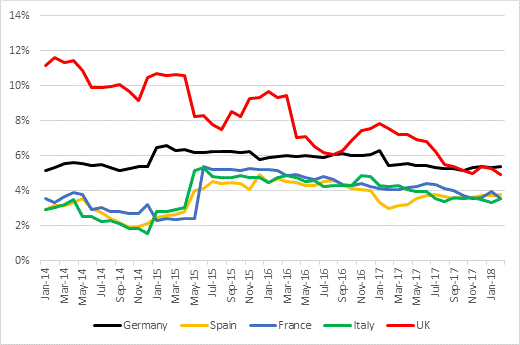

The upshot is that SUV values have broadly tracked overall market performance in recent years and there are even signs that values are now starting to fall. In fact, except for Spain, residual values for SUVs were lower in February 2018 than a year earlier. Moreover, the values of SUVs have failed to track the performance of average national values in the EU5 over the same period and even in Spain, the gap has only widened by less than one percentage point.

Difference in SUV values vs national average, EU5, 36 months/90,000km, Jan 2014 – Feb 2018SUV outlook

While demand for SUVs remains robust, the segment does face a number of challenges over the next 3-5 years. First and foremost among these is reducing their environmental impact. SUVs are typically larger and heavier than traditional passenger cars, which means they have greater fuel consumption and emissions. There is also the perception that, being heavier, they need to have the greater torque that diesel engines provide. In conjunction with the broader market shift away from diesel, the surging demand for SUVs has seen average CO2 emissions rise in markets such as the UK, France and Germany for the first time in years. As pressure grows to reduce emissions, then manufacturers will need to focus on cutting average fuel consumption for SUVs to stay relevant. BMW and Jaguar have already announced plans to introduce electric SUVs for example and Porsche is expected to follow suit after ceasing production of diesel derivatives of its models. This also has implications for the residual values of SUVs, especially as residual value growth is forecast to slow across the EU5 and many markets are even facing a decline in values.

Taking this into account, while growth in demand for SUVs is a consistent phenomenon across the EU5, the residual value outlook is rather mixed. Autovista Group analysts and editors highlight the following in the latest forecast round:

Germany: residual values are already very high and so we are conservative about the outlook. New entrants in this segment will reduce the average model age but values may have already peaked. This mirrors the pattern in the wider market; strong new car sales in all segments over the past few years will result in greater numbers of used cars being returned to the market in 2018 and 2019, resulting in residual value declines. Nevertheless, the various SUV segments are expected to perform slightly better than other segments with the decline being 0.1% in 2018 and 2019 compared with an overall 0.4% reduction in values. However, we anticipate a distinct shift from diesel to petrol and this is reflected in the forecast, with diesel values falling by 1.5% in 2018 and 1.4% in 2019 whereas petrol SUV values will enjoy modest gains.

Spain: residual values have been running high for several years, as economic growth has fuelled renewed demand for vehicles at a time when there is a shortage of supply. However, values are forecast to undergo a slight correction in 2018 and 2019. SUVs have seen a strong performance from a residual value perspective and new models will enter the segment but the willingness to pay a premium for these cars will not increase in Spain over the next 1-2 years. In fact, values for SUVs will fall at a slightly quicker rate than in the wider market, between 0.5% and 0.7%. We expect a stable value development for petrol SUVs but a downward trend for diesel SUV values in line with the other segments.

France: SUV residual value performance is expected to be positive but weaker than for the market overall. There are more and more competitors in this segment which limits the potential for growth. Mid-sized models in the C-SUV and D-SUV segments are predicted to deliver growth of between 0.5- 1.5% for 36 month old vehicles. This is more in line with the overall French market picture for 2018 and 2019. However, valuations for the smaller B-SUV models are expected to be weaker, underperforming the market as a whole. Valuations of 36 month old models in the E-SUV segment will be boosted in 2018 as new versions of the Audi Q7 and Volvo XC90 begin to filter through to the used car market but valuations will then stabilise in 2019.

Italy: SUVs are forecast to continue to deliver strong growth, even outperforming the wider used car market. Average residual values are expected to climb by 0.7% for young used cars in 2018 and 2019 and by about 1.0% for 36 month old cars. We predict that SUV values will gain 1.3% each year for 12 month old SUVs and by 1.8% for 36 month old vehicles. It must be noted, however, that diesel is not under as much pressure in Italy as in the other markets and so there will be less impact on the demand for used SUVs, and in turn their values, unless the regulatory environment changes.

UK: the SUV sector continues to be the fastest growing part of the new car market. Residual values in the C-SUV segment look set to decline slightly, but most other SUV segments are expected to turn in a static performance. This generally lacklustre picture is broadly in line with developments across the whole used car market but values for younger SUVs will underperform as increased supply better satisfies demand. We believe the segment is reaching saturation point with large volumes expected back into the market over the next 18 months, which will begin to erode values.