Monthly Market Update: Stock days and RVs fall in July

05 August 2024

Stock days fell across European used-car markets in July, but so did residual values (RVs). Experts from Autovista Group (part of J.D. Power) explore these declines with Autovista24 editor Tom Geggus.

Major European used-car markets saw the average number of days needed to sell a two-to-four-year-old car fall last month. Spain witnessed the greatest decline, down 12.3 days compared to July 2023, reaching 61.8 days on average.

The fastest sales were recorded in the UK, where stock was sold after 35.2 days on average. This was down by 6.3 days year on year. One of the longest periods was recorded in Switzerland, at 77.8 days. However, this was still 3.5 days faster than a year ago.

Shrinking stock days can indicate increasing demand. The sales-volume index (SVI) did post year-on-year improvements in Austria, Spain and the UK. However, Germany Italy and Switzerland saw overall retail activity drop compared to July 2023.

RVs still under pressure

A more consistent trend observed across these markets has been declining RVs of three-year-old cars at 60,000km. Values presented in absolute terms and as a percentage of retained list price (%RV), have fallen year on year.

The UK saw one of the steepest year-on-year %RV declines, dropping 12.5 percentage points (pp) to an average of 50.1%. Germany was not far behind, with a market-wide average of 49.9%, down 7.3pp. Spain recorded a more positive result, with three-year-old cars retaining 59.8% of their original list price. However, this was still down on July 2023’s result of 62.3%.

RVs continue to feel the weight of various different pressures across Europe. This includes consistent supply and inconsistent demand. Aggressive new-car pricing strategies are harming the values of models already on the market. In some cases, more cautious consumer activity is stalling purchases as buyers wait for prices to sink even lower. Rapidly advancing new-car technology is also dating older vehicles more quickly, lowering their perceived value.

Autovista Group experts expect these market pressures to persist. By December 2024, %RVs are forecast to be down across Austria, France, Germany, Italy, Spain, Switzerland, and the UK. However, this descent is then anticipated to slow in the following years.

The interactive monthly market dashboard examines passenger-car data by fuel type, for Austria, France, Germany, Italy, Spain, Switzerland, and the UK. It includes a breakdown of key performance indicators, including RVs, new-car list prices, selling days, sales volume and active-market volume indices.

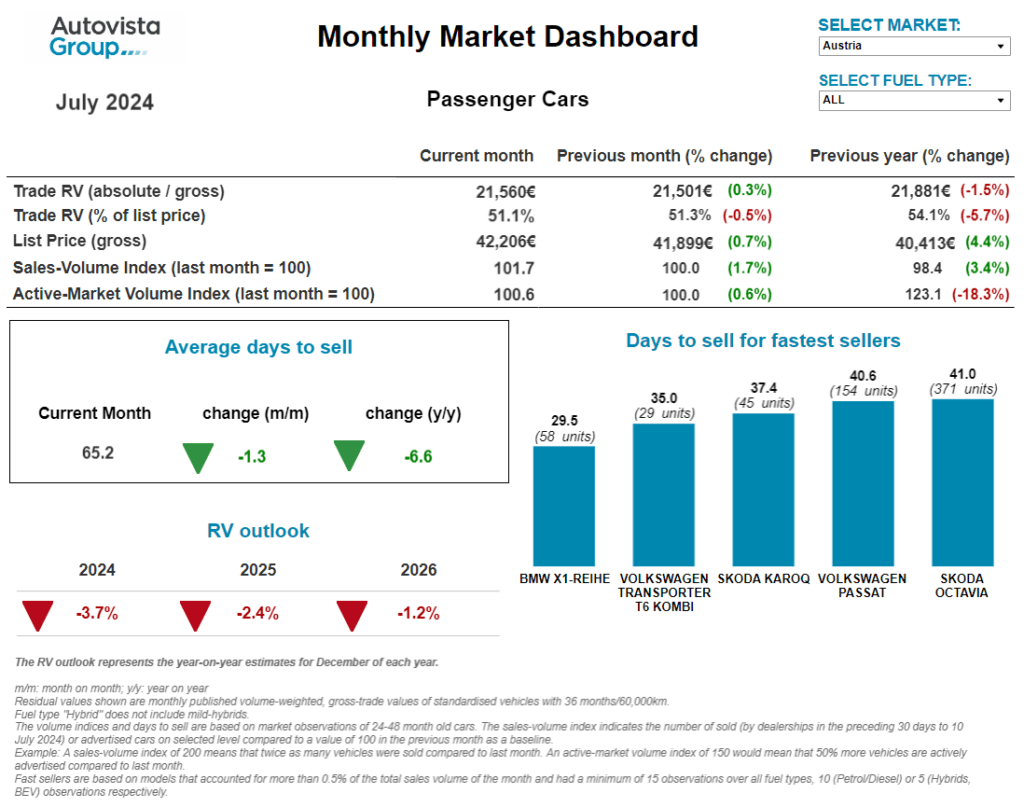

Marginal recovery in Austria

‘After falling in June, the SVI in Austria made a marginal recovery in July,’ highlighted Robert Madas, Eurotax (part of J.D. Power) regional head of valuations, Austria, Switzerland, and Poland. ‘The number of observed sales increased by 1.7% compared to the previous month and 3.4% year-on-year.’

Meanwhile, the supply volume of two-to-four-year-old passenger cars slightly increased by 0.6% compared to June. However, the supply volume of passenger cars in this age bracket dropped by 18.3% compared to the previous year.

At 65.2 days, the average amount of time needed to sell a used car fell slightly in July. Diesel vehicles continued to be the fastest-selling powertrain, averaging 58.1 days. This was followed by petrol vehicles at 67 days, hybrid-electric vehicles (HEVs) at 68.4 days and plug-in hybrids (PHEVs) at 69 days. Battery-electric vehicles (BEVs) continued to take the longest amount of time to sell at 86.4 days.

RVs of 36-month-old cars presented as a percentage of the original list price (%RV), sat at 51.1% on average in July. This equated to a marginal decrease of 0.5% compared to June, but a larger drop of 5.7% compared with the same period in 2023. This illustrates the increasing pressure on RVs.

‘HEVs retain the greatest amount of trade value at 56.9% followed by petrol cars (53.1%). Then came diesel models (50.7%) and PHEVs (48.5%). BEVs once again retained the lowest amount of value, at 43.9%,’ Madas explained.

In 2024, %RVs are expected to drop further by around 3.7% year on year. Due to weakening demand and unwavering supply, further pressure on values can be expected. In 2025 and 2026, %RVs are forecast to decrease at a slower pace.

Consumers wait in France

France saw RVs continue to drop in July in both absolute and percentage terms. This negative development was recorded across all powertrains, but BEVs recorded the largest decline. However, this did mean a slight boost in used sales, even amid weakening demand.

As of December 2023, electric car purchase incentives became dependent on lifetime carbon emissions, removing the eligibility of some brands. Therefore, used plug-in models are still too expensive, which is why prices have been dropping month after month. Where demand does not meet supply, the market sees a strong RV drop and lower prices.

‘PHEVs saw RVs fall again in July, with this descent picking up speed after June’s drop,’ said Ludovic Percier, Autovista Group residual value and market analyst for France. ‘This has been a consistent trend over the last few months and used PHEV volumes are not increasing.’

With its fleet-based benefits, the powertrain is better suited to the new-car market, while demand for used models flags. Newer PHEVs also feature more advanced technology and improved ranges at lower list prices, directly impacting the used market.

HEV values kept falling last month too. Despite recording the best market performance at the beginning of 2024, buyers appear unwilling to entertain such high prices. ‘People in France are simply not ready to pay the premium price for HEVs at the moment,’ Percier commented.

Demand for used diesel and petrol-powered cars dropped in July, aligning with the global fall of the internal-combustion engine (ICE). Yet, this decline is less worrying than the one experienced by BEVs and PHEVs.

‘This illustrates the overall descent of the French used-car market,’ Percier added. ‘This was confirmed by the SVI in July which fell once again. Consumers are clearly waiting for prices to drop further.’

RVs under pressure in Germany

In the first half of 2024, Germany recorded 3.2 million used-car transactions. This was up 8.5% year on year, meaning the market growth is still on track. The increase is particularly noticeable for BEVs and HEVs. The SVI for BEVs more than doubled last month compared to July 2023 as transaction activity continued to accelerate.

‘HEVS and PHEVs were also traded in greater volumes compared with 12 months ago. However, this positive performance was only enjoyed by electrified models. The overall used car transaction activity fell by 9.2% month on month and 4.8% year on year,’ Madas pointed out.

Supply is currently meeting with subdued demand, leading to a slight month-on-month increase in average stock days. In July, it took dealers 57.8 days on average to sell a used car. PHEVs and diesel-powered models sold the fastest at 53.6 days and 54.1 days respectively. Then came petrol cars after 58.3 days and HEVs after 62.5 days. BEVs took the longest amount of time to sell at 69.6 days.

Despite weaker demand, the average RV of a 36-month-old car remained stable. Expressed as a percentage of retained list price, models held on to 49.9% of their value. This equated to a marginal month-on-month increase, but a considerable descent from 57.2% recorded in July 2023, confirming increasing RV pressure.

HEVs led the way with a %RV of 54.3%. Then came petrol cars at 51.6%, diesel models at 50%, then PHEVs at 45.8%. Meanwhile, 36-month-old BEVs retained the lowest level of value at 39.6%.

‘As demand weakens and supply persists, RVs can be expected to come under even more pressure,’ Madas said. This year, %RVs are expected to fall further, dropping by 8.5% when compared with December 2023.’

Values fall in Italy

‘Italy saw RVs fall further than expected in July,’ stated Marco Pasquetti, head of valuations, Autovista Group Italy (part of J.D. Power). ‘This was despite the presence of a downward trend that had been apparent for several months.’

After a year-on-year decline of 3.6pp in June, %RVs hit 51.1% last month, down 4.2pp from July 2023. This descent can be expected to slow slightly towards the end of the year.

A 5.8% decline is forecast in December, however this is based on an already weak December 2023. Values started falling in September 2023, meaning comparisons will begin appearing more favourable.

As observed in recent months, only cars powered by liquid-petroleum gas (LPG) and compressed-natural gas (CNG) have escaped this decent. %RVs of CNG models enjoyed growth of 6.6% year on year while LPG values increased by 5.2%.

‘Rising costs of natural gas in recent years considerably reduced interest in the powertrain. However, now fuel prices have stabilised, buyers are beginning to take an interest in these vehicles again,’ Pasquetti added.

PHEVs and BEVs recorded the greatest year-on-year %RV drops, down 13.1% and 9.9% respectively. Enthusiasm for these powertrains is even weak on the new-car market, despite attractive economic incentives. This is illustrated by a weak market share, with both BEVs and PHEVs unable to claim a double-digit market share.

Rental channel fuelling Spain

The Spanish new-car market is very slowly moving towards its goal of one million units. This target will likely be reached thanks to a boost from the rental-car channel, which continued to sustain growth in June. In total, 535,243 units were registered in the first half of 2024, up by 5.9% year on year.

‘In this context of moderate growth, PHEVs and BEVs continue to see a slowdown in registrations,’ explained Ana Azofra, Autovista Group head of valuations and insights, Spain. ‘This means Spain’s electrification keeps moving further away from the European average.’

In the first half of 2024, these electric vehicles accounted for 10.4% of new-car deliveries, down from 11% a year earlier. Hybrids, including HEVs and MHEVs variants, continue to be unstoppable and closed the first half of the year with a growth of 25.8%.

In the used-car market, transactions exceeded one million units between January and June, up by 7% year on year. As mentioned in previous months, the pull of the rental channel is fuelling the young-used-car market. Recent years have seen transactions reshaped with a younger age profile, pushing the price of these models downwards.

‘On the other hand, residual values of middle-aged used cars are relatively stable,’ Azofra commented. ‘BEVs are the exception to this rule, as they have been following a far more negative trend. This is because of price reductions on the new-car market as well as significant discounts.’

The average %RV of used cars in Spain saw a marginal gain from June to July, up to 59.8%. However, this was a drop of 2.5pp year on year. HEVs retained the highest %RV last month at 65.3%, followed by petrol and diesel with 60.8% and 57.7% respectively. PHEVs kept 56.3% of their original list price, while BEVs retained just 49.6%.

No supply recovery in Switzerland

While supplies of used cars have returned to a pre-COVID-19 level in Switzerland, volumes are now falling slightly. Since 2023, the cost of living in the country has risen while new-car registrations have not bounced back.

The active-market volume index (AMVI) for two-to-four-year-old passenger cars fell by 0.3% from June to July 2024. Compared to July 2024, this indicator dropped by 11.3%. This shows that the supply of younger used models has not recovered. The SVI dropped by 5.1% month on month and 20.3% year on year.

‘Influenced by lower supply and stable demand, RVs of 36-month-old cars effectively remained stable,’ said Hans-Peter Annen, head of valuations and insights, at Eurotax Switzerland. ‘%RVs increased slightly from 47.4% in June to 47.5% in July. However, the year-on-year drop was still severe, as the %RV level sat at 50.5% in July 2023.’

HEVs retained the most value in July with a %RV of 51.1%. Then came petrol cars (48.5%), diesel models (46.5%) and PHEVs with 45.1%. BEVs were once again the worst-performing powertrain, retaining only 42.8% of their original list price.

July saw two-to-four-year-old passenger cars sell more quickly. Time in stock shrank to 77.8 days on average, down 5.7 days compared to June. HEVs sold the fastest at 70.4 days, followed by petrol cars after 73.1 days and diesel cars after 74.9 days. PHEVs took 88.8 days to sell and BEVs needed 100 days on average.

‘Set against a wider declining trend, the values of three-year-old cars are forecast to keep falling from an already high point. Last year saw %RVs fall 5% year on year. By the end of 2024, used-car values are expected to drop by 4.6% due to stable supply and conservative demand,’ Annen added.

UK rollercoaster ride

In July, the average three-year-old car retained 50.1% of its original cost-new price in the UK. Absolute trade RVs hit £15,188 in the month, down £2,313 on July last year. RVs have fallen in every edition of Glass’s data over the past 12 months. Values now sit at a similar level to July 2021, just before prices rose significantly.

‘At the time of writing, both wholesale and retail activity has improved in the UK. So, the roller-coaster ride for used-car values may be coming to an end, with greater stability on the horizon,’ said Jayson Whittington, Glass’s (part of J.D. Power) chief editor, cars and leisure vehicles.

‘The SVI revealed an increased rate of sales, up 10.3% between June and July. Meanwhile, the AMVI revealed only a 0.7% increase in car adverts,’ Whittington added.

It seems sales activity has begun to outpace the growth of available forecourt stock, which should give dealers the confidence to source additional inventory. This already seems to be happening with a recent uptick in auction activity and an improvement in hammer prices.

The average time it took a dealer to sell a used car increased by 1.7 days compared to June’s dashboard. This might be surprising given the increased sales rate, but this is likely a result of fewer fresh cars hitting advertising portals.

Entering the summer period, dealers seem to be approaching the acquisition of fresh stock with caution. This time of year often sees lack-lustre retail activity. However, the summer of 2024 has so far enjoyed reasonably good levels of activity. Compared to July last year, the average number of stock days has fallen by over six days.