Light at the end of the tunnel for Swiss passenger-car registrations

15 December 2022

Hans-Peter Annen, head of valuations and insights Switzerland at Eurotax (part of Autovista Group), examines the Swiss automotive market.

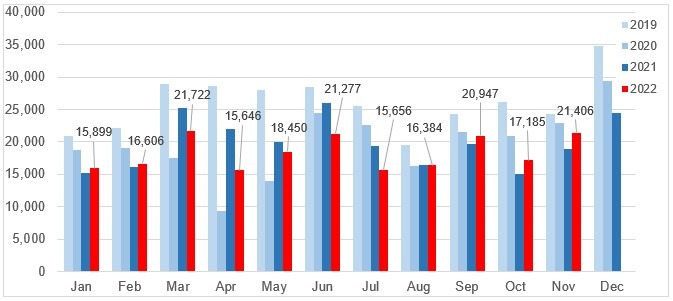

New-car registrations in Switzerland continued to develop positively in November, also improving on the previous year. This means the 2022 year-on-year decline has slowed. Despite the war in Ukraine, supply chain uncertainties, inflation and energy fears, a further slight recovery is expected in December.

In November, 21,406 new passenger cars were registered, up 13.7% year on year. However, this is an 11.7% decline against the pre-COVID levels of 2019. The first 11 months of 2022 were down 6% year-on-year, and down 27.3% versus the same period in 2019. The share of so-called ‘alternative drive systems’ including mild hybrids now sits at almost 55%.

Swiss new-car registrations by month: 2019-2022

Meanwhile, the used-car market has been on a high since the summer of 2020, underpinned by stable demand combined with low supply, but supply is now increasing again. Last year, used-car transactions inched up by 1.1% to 840,044, almost reaching the pre-pandemic levels of 2019. In the first half of 2022, however, changes of ownership took a strong hit and were 8.5% below 2021 (according to the previous counting method).

Under the new counting method, the figures for the first 11 months of 2022 are even more clearly below 2021 but are no longer directly comparable. Therefore, the upward trajectory was broken this year. The trend towards declining changes of ownership is likely to continue as long as new-car registrations remain low, while fears of a recession begin to creep in.

Swiss used-car transactions by month: 2019-2022

Since the beginning of 2022, the Federal Roads Office ASTRA provides figures for changes of ownership. Before that, up to and including June 2022, ASTRA supplied raw data with all changes in Switzerland’s vehicle stock. The analysis of changes of ownership was carried out by Eurotax, partly with assumptions. The figures calculated in this way were approximately 3% higher than the volumes according to ASTRA’s new evaluation from 2022 onwards. For this reason, the figures shown for 2022 are based on ASTRA data. The volumes up to and including 2021 are shown according to the previous method. When comparing the figures for 2022 with previous years, this must be taken into account. Comparisons are therefore only possible to a very limited extent, if at all.

Although the number of used cars on offer has recovered steadily in recent months, the volume is still around 7% lower than in February 2020. Offer prices for diesel and petrol models have benefited particularly from this shortage. Plug-in hybrids (PHEVs) and, above all, full hybrids (HEVs) were also able to make gains, albeit to a lesser extent. In the meantime, the price trend is either down slightly or consistent.

Battery-electric vehicles (BEVs) are struggling to return to 2020 levels across all age groups. However, younger models are an exception. Among 12-month-old cars, BEVs (together with HEVs) take first place in terms of RV retention, with a retail value of 83.5% on average.

With lockdowns and factory closures reoccurring in China, the Ukraine crisis leading to exorbitant energy costs, and supply chains still disrupted, new-car sales are also unable to make a significant recovery. This continues to affect supply and used car prices, which are flattening out or declining slightly, albeit at a high level.

The supply situation, also in comparison to consumer sentiment and demand, is crucial for the future development of the used-car market. Residual values are only likely to come under pressure if used-car demand drops significantly due to the gloomy economic outlook and supply fears. In the meantime, they will remain at a high level.