UK used-car market looking bright for rest of 2021

29 July 2021

Jayson Whittington, chief editor at Glass’s (part of Autovista Group) considers how the UK used-car market is shaping up as lockdowns end.

The UK used-car market experienced exceptionally strong demand in the second quarter of 2021. This followed a lack-lustre first quarter, brought about by the country’s third national lockdown. The outlook for the rest of this year appears positive, although used-car stock supply is becoming a concern, says Whittington.

In part, the stock shortage is due to the impact of lease-contract extensions and a lower level of dealer part exchanges, both caused by delays in new-car supply. A reduction in short-cycle business throughout last year is also affecting the supply of younger used cars.

A total of 1.63 million new cars hit UK roads in 2020 according to the Society of Motor Manufacturers and Traders (SMMT). With over 680,000 fewer cars registered, last year experienced the lowest total volume since 1992. The UK’s first national lockdown accounted for a significant proportion of the losses, with the new car market down over 615,000 units by the end of June.

A reduction in rental registrations resulting from the collapse of the travel sector was noticeable. The UK welcomed significantly fewer overseas visitors, leading to rental vehicles being underutilised. With little prospect of the situation changing in the short term, rental companies did not renew their fleets to the same level as in previous years.

Perfect storm

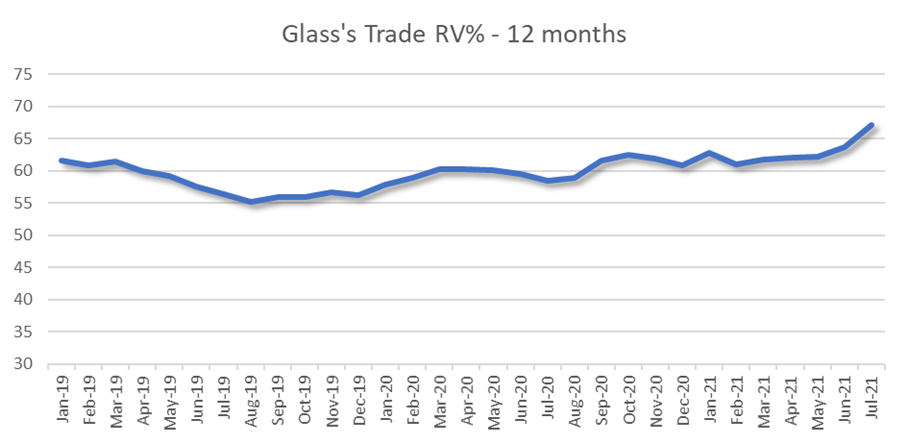

Fast forward 12 months and the used-car market is feeling the impact of this, with a hole in the supply of young used cars. Add to this, increased interest in them due to new-car production delays, and you have a perfect storm leading to an uplift in residual values (RVs), says Whittington.

Source: Autovista Group Residual Value Intelligence (RVI)

The outlook is similar for the supply of three-year-old used cars due to lease extensions; however, the full impact will be felt in 2023/24, with fewer cars expected to terminate than in a typical year due to 2020’s low registration volume. Autovista Group’s residual value outlook predicts that three-year-old cars will depreciate at a slower rate in 2023, although battery-electric vehicles (BEVs) will experience a more turbulent time, as recent registration spikes resulting from attractive benefit-in-kind taxation for company-car drivers, and could lead to supply in the used-car market significantly exceeding demand.

Lockdown subdued market

This year began with the UK experiencing its third national lockdown, badly impacting the automotive market until easing began in mid-April. Whilst consumers had access to ‘click and collect’ throughout this period, both new and used car sales were subdued. This underlines the UK car industry’s continuing reliance on a physical sales process, with the old adage of ‘bums on seats sells’ still being relevant in today’s market, observes Whittington.

As restrictions eased, the wholesale used-car market spluttered back into life, although it took until the latter part of April for activity to ramp up. That said, ever since, it has not stopped and continues to strengthen.

Under the hammer

Auction hammer prices were strong throughout May but strengthened further in June, leading to unprecedented rises in RVs, as Glass’s reflected the spike in wholesale activity. In May the volume of cars that sold on the first time of asking at auction was 85.3%, which was the highest first-time conversion rate since July last year, which was at the height of the bounce-back that followed the end of the first lockdown.

In June, 84% of cars sold first time, however focusing on younger used cars, it is clear to see that current demand is exceptionally strong, with cars up to two years of age achieving a first-time conversion rate of 95%, reflecting the reduced volume in the market.

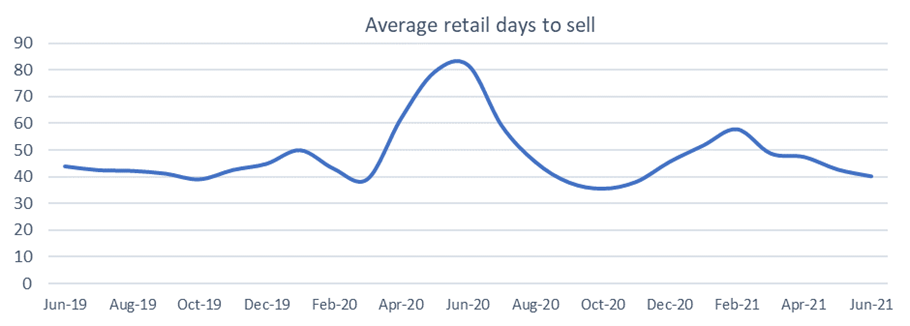

The strength in the UK wholesale market is underpinned by strong and consistent retail demand. The amount of time a car spends on the forecourt is generally a good barometer for the health of the used-car retail market. Unsurprisingly, the UK lockdowns played havoc with this figure over the last 18 months, but the good news is that the average has improved noticeably since the easing of restrictions. June’s average of 40 days is an improvement of 2.6 days from May and comfortably below the average for June 2019.

Ordinarily, demand begins to slow in the summer months as consumer focus switches towards holidays. However, May and June’s exceptional activity has intensified in July. It is possible that potential buyers are reflecting on the prospect of limited or at least uncertain overseas trips this summer, with some choosing to use unexpected disposable income on changing their car, which both new and used-car dealers will welcome.