UK new-car market ends 2022 with further improvement

06 January 2023

UK new-car registrations rounded off 2022 with their fifth consecutive month of year-on-year growth. Moreover, the market strengthened modestly, in line with Autovista24’s expectations for December, senior data journalist Neil King explains.

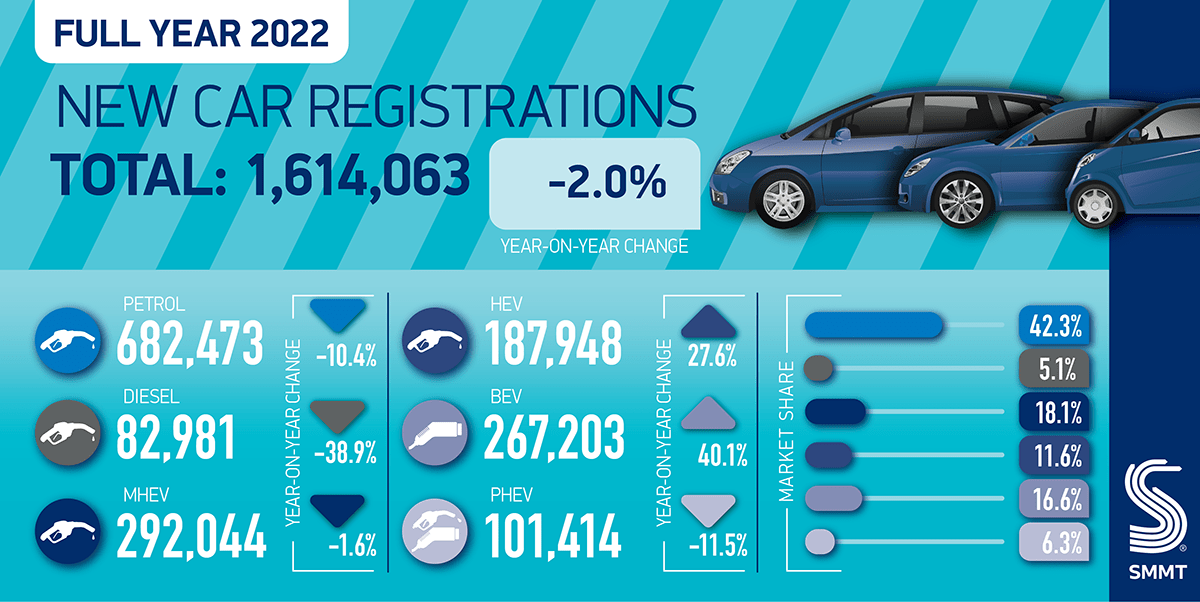

The Society of Motor Manufacturers and Traders (SMMT) reports that new-car registrations increased 18.3% year on year last month, to 128,462 units. This appears weaker than the 23.5% growth in November but there was one less working day than in December 2021.

Adjusted for working days, Autovista24 calculates that the market gained 24.2% year on year and that the seasonally-adjusted annualised rate (SAAR) improved to 2.12 million units from 2.08 million units in the prior month.

However, the SMMT emphasises that the performance of recent months did not ‘offset the declines recorded during the first half of 2022. Despite underlying demand, pandemic-related global parts shortages saw overall registrations for the year fall 2% to 1.61 million, around 700,000 units below pre-COVID levels.’

On a more positive note, the SMMT added that ‘Britain reclaimed its position as Europe’s second largest new-car market by volume’ – exceeding France for the first time since 2019.

Forecast held

The consumer prices index (CPI) receded slightly to 10.7% in the 12 months to November 2022 but the Bank of England increased interest rates by 0.5% to 3.5% on 14 December. Furthermore, the average energy price cap will increase from £2,500 (€2,900) to £4,500 (€5,220) from April 2023, and unemployment is expected to rise too.

The cost-of-living crisis shows no sign of abating and although the supply situation continues to improve, the semiconductor shortage is unlikely to disappear in 2023. The outlook for the UK’s new-car market remains particularly uncertain, but as it continues to perform in line with Autovista24’s expectations, the 2023 forecast of 13.3% growth to 1.83 million units remains. This would be 20.9% lower than in 2019.

‘Looking ahead, supply chains are beginning to stabilise and although the shortage of semiconductors is expected to ease, erratic supply will likely impact manufacturing throughout 2023. The most recent [SMMT] market outlook, published in October 2022, anticipates around 1.8 million new car registrations in 2023, worth around £8.4 billion in additional turnover,’ the SMMT noted.

The downside of recovering supply is that new-car registrations will be less bolstered by fulfilling a backlog of orders. Furthermore, new-car demand will continue to suffer from weak consumer confidence, high interest rates and inflation. Against this backdrop, Autovista24 has maintained its year-on-year growth forecast for 2024 at 4.8%, taking the market to 1.92 million units.

Diesel relegated to fourth place

Despite the UK government’s termination of the plug-in car grant (PiCG) on 14 June, the SMMT highlighted that ‘constrained supply saw many manufacturers prioritise deliveries of the latest zero emission-capable models. December saw battery-electric vehicles (BEVs) claim their largest ever monthly market share, of 32.9%, while for 2022 as a whole they comprised 16.6% of registrations, surpassing diesel for the first time to become the second most popular powertrain after petrol.’

Registrations of new plug-in hybrids (PHEVs) gained just 0.4% year on year in December, with their share falling to 6.5% in the month and 6.3% in full-year 2022, replicating the downward trend across Europe. Nevertheless, electric vehicles (EVs) accounted for almost 40% of new cars registered last month and 22.9% in the year as a whole.

Hybrid-electric vehicles (HEVs) enjoyed the fastest year-on-year growth (58.1%) of all powertrains in December, commanding a 10.7% market share. Moreover, they captured 11.6% of the market in 2022, relegating diesel (including mild-hybrid diesels) to fourth place.

Fair taxation and charging infrastructure

As the share of new cars powered by internal-combustion engines (ICE) is in sharp decline, governments need to address the shortfall in their finances by not only reducing incentives for EVs but also taxing them.

In July 2022, Switzerland outlined plans to tax EVs and in the 2022 autumn statement, the UK government announced that EVs will no longer be exempt from vehicle excise duty (VED) from 1 April 2025. ‘This will ensure that all road users begin to pay a fair tax contribution as the take-up of electric vehicles continues to accelerate.’

The SMMT has cautioned that ‘while the industry recognises the need for fair vehicle taxation, plans to introduce VED on BEVs from 2025 with the same ‘premium’ threshold as internal combustion-engine cars will disproportionately penalise those moving to electric. Higher production costs mean more than half of all BEV registrations this year would have incurred the ‘premium’ VED if it had been in place, a move which risks discouraging wider adoption.’

Furthermore, the SMMT emphasises that the UK’s charging infrastructure ‘remains a barrier to EV uptake’ – especially for private buyers. ‘The government’s EV Infrastructure Strategy forecast that the UK would require between 300,000 and 720,000 chargepoints by 2030. Meeting just the lower number would still require more than 100 new chargers to be installed every single day. The current rate is around 23 per day.’

‘Manufacturers’ innovation and commitment have helped BEVs become the second most popular car type. However, for a nation aiming for electric mobility leadership, that must be matched with policies and investment that remove consumer uncertainty over switching, not least over where drivers can charge their vehicles,’ concluded SMMT chief executive Mike Hawes.