Sales of new and used-electric vehicles to grow in 2022, but challenges abound

01 February 2022

While the automotive industry is on a fast track to electrification, questions remain about the strength and viability of electric sales in both new- and used-car markets.

Every carmaker is unveiling new electric models or plans to reduce and end the production of internal-combustion engine (ICE) vehicles. Gigafactories are being built across the continent, and technology providers are continuing a pace to bring more relevant systems to the market – ones that emulate and improve upon decades of ICE rule.

But does this progress help or hinder the market for battery-electric vehicles (BEVs) and plug-in hybrids (PHEVs), especially in the used-car market? For the used market, there’s challenges. New automotive technology, improved ranges, and faster charging times for newly-launched electrically-chargeable vehicles (EVs) are likely to put pressure on EVs when they reach the forecourts of used-car dealerships across Europe.

In addition, numerous masking and economic factors are still at play. The COVID-19 pandemic impact may be much lower than it was throughout 2020 and 2021, but the automotive market is still suffering. Add in a new variant such as Omicron and a pattern of easy disruption is unveiled. With a car being undoubtedly one of the biggest purchases a consumer makes, and with new-EV prices still very high, this is a segment that can see dramatic changes in a short space of time.

Europe the leader

The recent Autovista24 webinar: 2022 outlook – electrifying Europe’s new- and used-car market, charted the progress of the EV market in Europe to date and considered the issues and challenges building pressure on the used-car market.

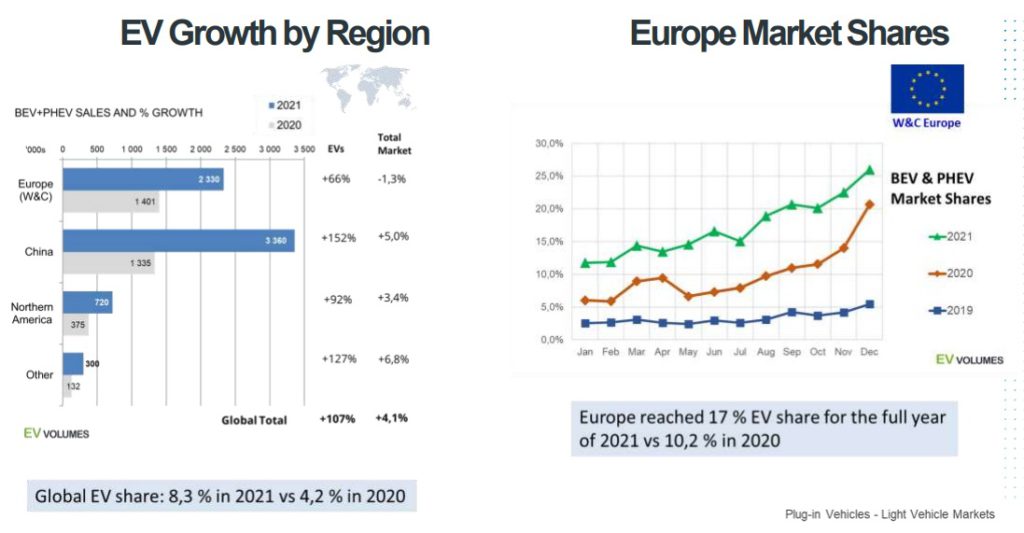

‘Europe was the driver in global EV sales in 2020, with sales outside the continent suffering more due to the COVID-19 pandemic,’ commented Roland Irle, managing director at EV Volumes, a panellist on the webinar.

‘Strong policies and incentives in the market helped to drive this growth, and with other regions picking up last year, total worldwide registrations equated to 6.73 million in 2021, or an 8.3% market share, he added.’

Currently, Tesla is the global market leader when it comes to BEVs. But the tech company, one of the pioneers of the EV revolution, has been unable to keep up with rapid demand in Europe. All models sold on the continent in 2021, totalling around 170,000 units, were imported from China or USA. Yet new gigafactories in Berlin, Germany, and Austin, US, will expand Tesla’s global capacity to 1.5 million units in 2022, meaning others will need to work hard to displace Tesla from the top of the sales charts.

Irle expects cost parity compared to ICE evolve in the market across the coming years. Sales of ICE models will decline and new gigafactories will power up across Europe and the US.

‘We expect around 9.5 million BEV and PHEV deliveries globally for 2022,’ Irle added. ‘Our outlook for 2030 sees 40% of global car sales being BEVs and PHEVs.’

Economics at play

Factors such as increased regulation of the automotive market, and awareness of environmental challenges, are helping drive electrification. However, this transition coincides with the pandemic and its related economic impacts.

This disruption has seen both new and used-car sales fluctuate wildly in the last two years. ‘Used-car markets still fared much better than new-vehicles markets,’ commented Christof Engelskirchen, chief economist, Autovista Group. ‘So, in relative terms, stakeholders in the used-car market did well. From a price-realisation perspective, the markets performed really positively over the past two years, and those that had cars to sell benefitted from this.’

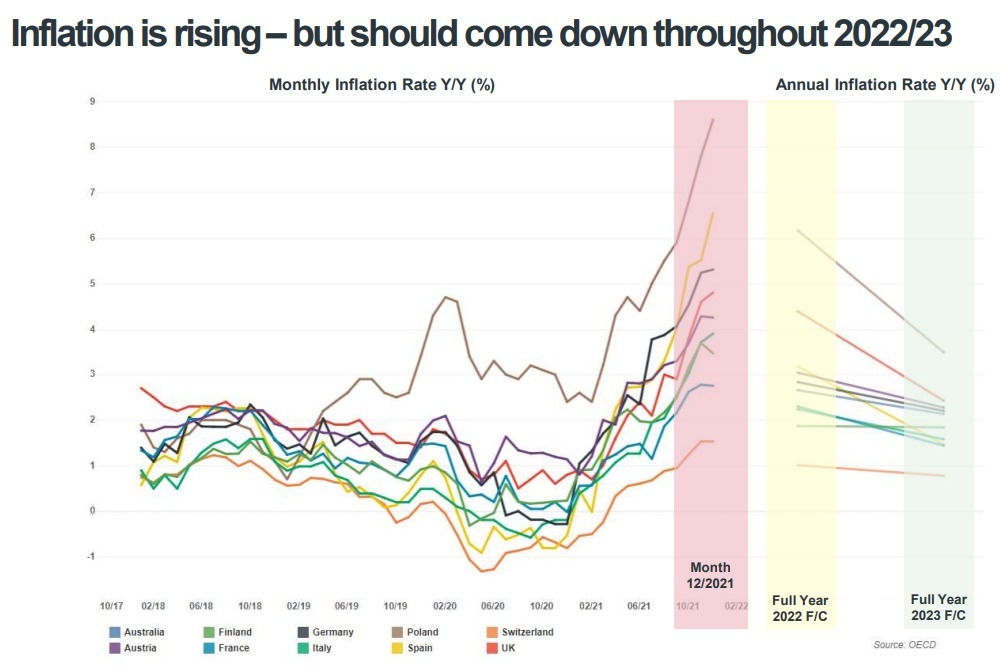

When it comes to rising car residual values (RVs), Engelskirchen highlighted that the UK was experiencing the most dramatic rise, thanks not just to COVID-19, but also the impact of Brexit and the ongoing semiconductor crisis. The UK also struggles as it is the only right-hand drive market in Europe, meaning used cars cannot be imported into the country to make up for a lack of supply. Elsewhere, Poland saw a strong economic rebound, which has affected both inflation in the country and the demand for used-vehicles.

‘Strong monetary and fiscal intervention has, so far, been supporting a rather quick V-shaped recovery,’ said Engelskirchen of the main European markets. ‘Forecasts improved over the past two years towards the speed of the recovery, but the recent COVID-19 Omicron variant has affected things. Rather than creating another wave, however, it has merely put a small “hockey stick” into the recovery trajectory. By the second quarter of this year, economies should have caught up again.’

Bubble build-up

A depressed supply of new vehicles and a rise in EV sales may not be enough to justify talks of a bubble when it comes to remarketing in the near term, but it is a scenario that could be building in the coming years.

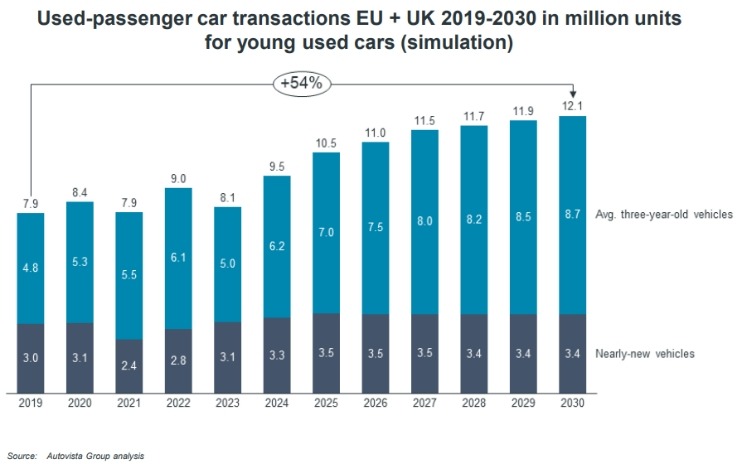

‘We expect the volumes of to-be-remarketed young used cars to rise by more than 50% by 2030,’ stated Sonja Nehls, principal analyst, Launch Intelligence, Autovista24. ‘With the rise of leasing and private contract purchases, holding periods decrease and that increases the number of young used vehicles entering the used-car market, from nearly new up to 36 months old. A bubble could very well be forming out of this.

Further development to come

The used electric-vehicles market is still not fully developed in Europe, with numerous challenges facing the industry. Infrastructure is not yet on a sufficient level in some countries for drivers to consider an EV purchase, and the new-car market is still heavily incentivised in various regions. ‘This remarketing risk is difficult to grasp and requires close observation and risk management,’ added Nehls.

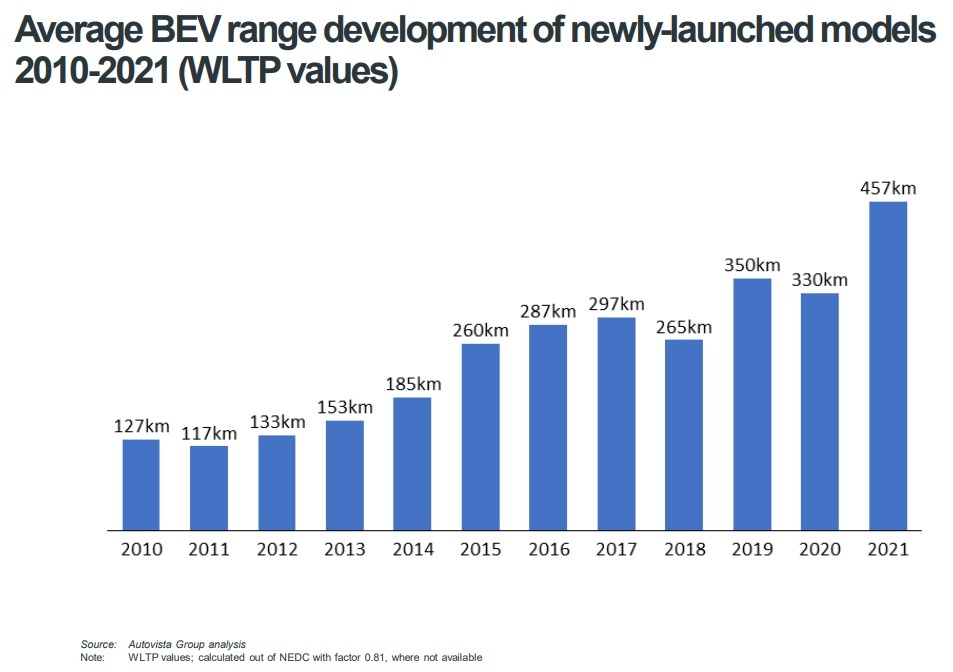

One challenge for BEV remarketing is lifecycle depreciation, which will continue to be higher than for ICE vehicles. The main reason for this is the high pace of technological developments, making older cars almost obsolete. ‘Over the past two years, the average range of a BEV has increased by 100km,’ Nehls highlighted. ‘That puts some realistic price pressure on used BEVs in the near future, until ranges in the used-car market are beyond 500km on average. Range is just one example, however, as upgrades to charging technology, and the introduction of features-on-demand in new cars pile pressure on older vehicles.’

Transcript – 2022 Outlook: Electrifying Europe’s new-and used-car markets

Phil: Hello and welcome to Autovista24’s latest webinar, the 2022 outlook electrifying Europe’s new-and used-car markets. I’m Phil Curry, Editor of Autovista24 and before we get into today’s discussion, I want to give you a brief overview of what Autovista24 is all about. We bring you analysis of latest topics and challenges facing the automotive industry through various different mediums, news features and data driven articles. We also have multimedia channels through podcasts and YouTube which allow us to dig deeper into the information that you need for your everyday businesses. We bring together the expertise of Autovista Group in one place to keep you informed about everything going on in the automotive market. You can visit us at autovista24.com and while you’re there don’t forget to sign up to our daily email which brings you everything you need to know directly to your inbox every morning.

Now, as part of Autovista24, we have also launched a new report. This has been published in January and focuses on automotive trends and growth opportunities for new-and used-passenger cars. It’s available now and the link is on screen now. Now, this report covers everything from electrification to ramifications for new and used car markets across Europe. Deep dive into segment trends for some of the most popular power trains, car residual values for the key markets in Europe and recommendations for OEMs, fleet and finance, dealers and governments. It’s a really interesting read so make sure you check it out and this slide deck will be available to you after this presentation. So, if you haven’t had a chance to take note of that URL, you will get to again shortly afterwards.

Now, electrification is really taking off. We’re seeing an increasing number of car makers announcing their electric-only plans. Regulations as well are really forcing the market down that route with current fit for 55 proposals suggesting 100% emissions reduction from 2035. There’s also increasing consumer focus on electrically-chargeable vehicles, battery– electric vehicles and plug-in hybrids. They’re also new brands coming through to market, new launches, new concepts all of which are embracing electrification. We saw quite a lot of this recently at CES2022 with a number of car makers highlighting new automotive technology. Everything from small quad recycles right up to electric pickup trucks. One of the most interesting concepts was the Mercedes-Benz EQXX with a range of around 1,000 kilometers. It may only be a concept, but such technology, such ideas surely are on the drawing board for car makers and you can catch up with all of our CES coverage which covers a lot about electrification again on autovista24.com. If you click on our video channel you’ll find our presentation.

Now, today we’re going to be covering a number of topics and of course at the end of this you will get an opportunity to ask your questions about them. On the right-hand side of the screen is a box where you can put in your questions throughout the webinar. Don’t wait until the end if you see something, you hear something that’s of interest put it into the box. I may even interrupt our experts while they’re talking. We will do our best to respond to all unanswered questions after our Q&A session even if we don’t get time to answer them in this webinar. So, again make use of this opportunity when you can and at the end as well contact details of our experts will follow.

Now, our agenda today is going to take us through some really interesting topics as we look forward to 2022. We’ll look at the state of Europe’s electric vehicles market, marketing factors and economic strength, the risks of a bubble build up before a summary and the Q&A that I just mentioned and I’m really delighted to be joined by some of Autovista Group’s top experts today. We have Dr. Christof Engelskirchen who is Chief Economist at Autovista Group. Roland Irle who is a managing director at EV volumes and Sonja Nehls principal and analyst launch intelligence also at Autovista24. Thank you all very much for joining me.

Now, first of all we’re going to look at state of Europe’s EV market in the new vehicle market. Now, I’m going to come to you Roland. The market is currently seeing shares of almost 20% for battery-electric vehicles and plug-in hybrids, electrically-chargeable vehicles as a whole that’s quite a success story. It’s quite a rise especially over the last couple of years, but how surprised are you about this trajectory? Is the market at risk of overheating?

Roland: Almost probably not overheating. In terms of volumes, the growth in Europe was as expected. However, as the Europe auto sales stayed considerably below expectations, share came out higher 17% for the year. December saw a new record with 25% EVs in new car sales and in 2020 Europe was the EV growth motor with a sales increase of 138% from 2019 to 2020. In 2021 the increase stayed at 66% while the other regions grew even much faster.

Phil: Could you put into some context for us? What’s happening around us at the moment?

Roland: Well around the world EVs are growing at a very strong pace now and this is partly explained by the low base effect as EV sales outside Europe suffered more from the pandemic during 2020. Even if they were more resilient than the total car markets. With strong incentives and policies, Europe kicked off the EV boom in 2020 and in last year in 2021 the other regions made up for the stagnations they had seen during the 2020 pandemic and globally this added up to 6.75 million deliveries of EVs. 108% increase over 2020 and the 8.3% market share which is quite a lot.

Phil: So, what are some of the common drivers for the market? What’s happening to bolster these higher adoption rates around the world?

Roland: Well, we see some common denominators like the portfolio expansion in EVs from almost all OEMs with improved products, notably e-range at almost unchanged prices. Another important reason is charging infrastructure built out the higher priorities on EVs are getting in marketing and distribution and also exports. Then we have environmental concern and health concern. In particular now after these experiences we have increases in awareness and inexperience with EVs. They are more on the road, they are seen everywhere now. Oil prices are high, they are above pre-pandemic level now and they are often combined with higher taxes on fossil fuels and then we have the cost decline of renewable energy installations like solar panels and EV ownership that go hand in hand and as these motivators will mostly stay with us for the coming years we are very optimistic about future EV adoption.

Phil: Now, forecasters sometimes they can be wildly ambitious but in the case of EVs forecasts have been rising and rising for 20/30s particularly including yours. How ambitious are you compared to other forecasters and what’s the reason for that?

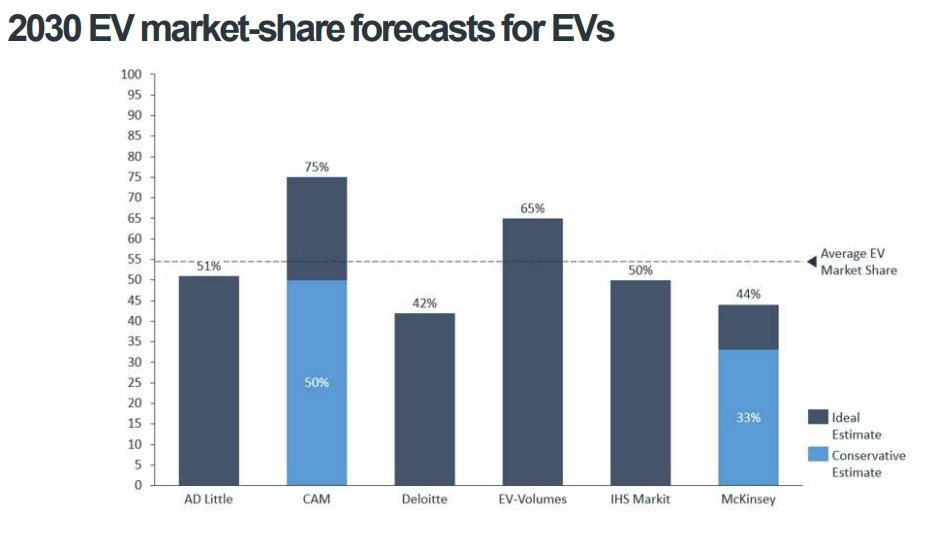

Roland: Well, we have been rather bullish about the EV potential since a long time and when we started EV volumes back in 2015, we were already looking back to five years of steady EV sales increase and product improvements as well. Sure enough we had to revise our forecast both up and down, but then the forecast is never one and done and we adjust continuously. You can show this chart.

Yes, this is an example for various 2030 EV forecasts for Europe including ours and in the early days of our company the picture would have been very different when our forecasts were a multiple of what traditional agencies were predicting. Today we are usually in the upper third of the forecast range.

Phil: So, what can we expect for 2022 as we’re discussing today and also for long term?

Roland: Well, for this year we are expecting 9.5 million BEV and PHEV deliveries globally which is another increase of 42% of the high increase we have seen this year. This will calm down, but we still will see a considerable increase maybe more if supply chain work and our outlook for 2030 is that around 40% of global light vehicle sales will be BEVs and PHEVs.

Phil: Now, we wouldn’t be talking about electric vehicles if I didn’t mention the ‘t’ word so Tesla. Will Tesla be as dominant in 2022 and 2023 as they were last year and what was the most exciting announcements that’s going to keep the industry really surging forward with everything?

Roland: Tesla has made the number one position this year again. Nine hundred and thirty-six thousand deliveries which is a clear number one and what we foresee is that they will retain this position for quite a while and in their current position they are constrained by supply and logistics and they could for instance not keep up with the rapid growth of EV sales in Europe. All Europe volumes of Tesla which was 170,000 last year is imported from either China or USA. Tesla is opening two factories this year. One in Berlin and one in Austin Texas and Tesla is increasing local capacity to approximately 1.5 million units for 2022 depending how the ramp up works out and by this they can keep and maybe even extend this sales lead. Midterm, new products in very large auto segments like pickup trucks in the US and compact SUVs worldwide will further solidify Tesla’s position.

Some exciting announcements I think we can look forward to is in the next year’s cost parity of EVs with ICE vehicles or EVs outselling their ICE counterparts. Spoiler alert, BMW 4 series and i4 Europe and USA battery plants going online in large scale among many other things, but these three I’m looking most forward to.

Phil: Excellent Roland thank you very much. We’re now going to move on to our next sector masking factors and economic strength. Now, before I come to you Christof, I’d like to come to you our audience instead. I’d like to get your opinions, your views in our survey. How concerned are you about risks of a bubble build up on Europe’s used car markets in 2022 and 2023? Very concerned, do you think prices have risen for used cars too much? Are you mildly concerned, some smaller down corrections maybe? Or not concerned at all, do you think that supply constraints may keep prices stable? So, we’re going to run this survey now. We’re going to keep this open for a minute or two. So again, just to reiterate there how concerned are you about the risks of a bubble build up on Europe’s used car markets in 2022 and 2023? And while we keep this on-screen I would just like to highlight that the slide deck and a video of this webinar session will be made available to you all at the end. So, I have no worries that if you missed any details, any links, if you want to see any of those charts again you can do.

You don’t have to be scripting down notes furiously. So, just keep this up on screen just for a little while longer. Again, be really good to hear your views or see your views on this subject. Okay, I think we can look at some results now. So, here we are. So, mildly concerned, some smaller downward corrections, 46% obviously leading the way there. Very concerned and not concerned 20%, It’s quite an interesting response rate actually though.

So, Christof, I’ll now come to you. We’ll see on the back of this the current market dynamics are not fantastic at the moment. Everything still seems to be very largely disrupted and it’s very difficult to predict as well. What are the masking factors that are affecting automotive markets at present?

Christof: Yes, this is a good question and one that we have been struggling with because there are so many factors at the moment that have such a high and disruptive impact on supply and demand that it’s so challenging right now to predict what’s going to happen and the ones that you can see on the screen at the moment there are other ones that will stay with us for a little bit longer. So, we have Covid19 which for example not only had this disruptive effect on suppliers, on supply chains across the world, but also on demand. So, the demand for cars was rising a lot over the past two years and supply couldn’t keep up. We’ve seen that strong monetary and fiscal intervention and the latest risk that has surfaced is inflation, but there’s also this you know more systematic risk now around chip shortage which has been with us for some time. It’s going to go away to some extent over the next 6-12 months, but when you see what suppliers are saying they keep mentioning the automotive industry. It’s just a very small you know fraction of those asking for better and improved chips. So, in the end this will stay with us for a little bit longer and the demand for chips will just keep on rising for other devices as well, not just cars and we have that European green deal which is such a powerful piece of industrial policy and a lot of the things that Roland just mentioned earlier are so much affected by Europe’s green deal rather than a superiority of the battery-electric vehicle for example, from a suitability for daily everyday use or from a pricing perspective. So, it’s very much driven by you know the carrot and stick approach and that Europe, the EU but also national governments are putting upon us.

Phil: Now, during the Covid19 pandemic we saw the new-car market fluctuate wildly at some point. The used-car market seemed a bit more stable, there was peaks and troughs but not as bad. Would you consider therefore that the used-car market was the winner in the pandemic?

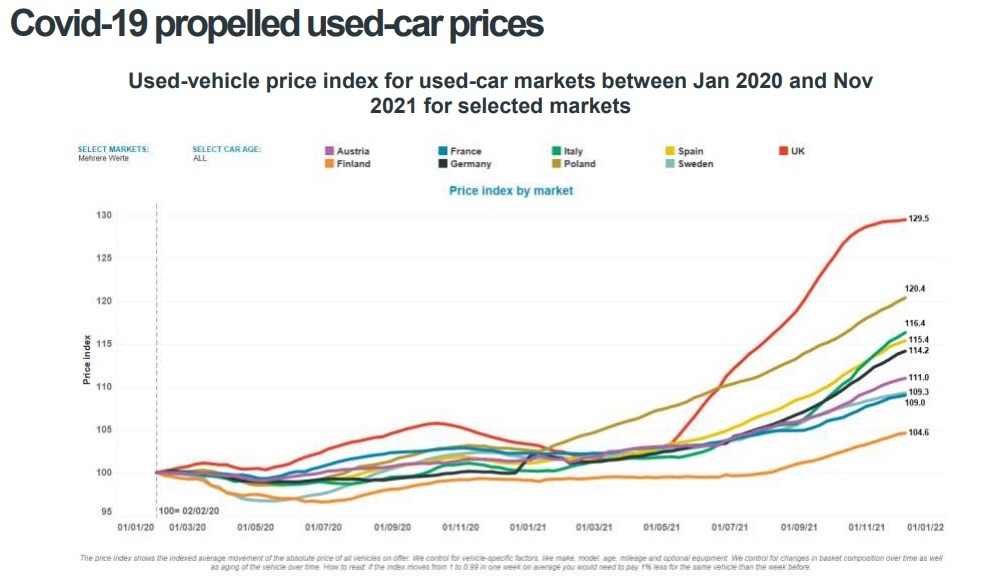

Christof: Yeah, I mean first of all the used market also suffered in terms of number of transactions. Not as much as the new-car market that was down or still is down 25% versus pre-pandemic 2019 levels, but what people are usually saying with regard to the used-car market is that they developed favorably in terms of prices because of the factors that we have just shown you on the page, but this chart in particular speaks to the Covid19 situation and how it has propelled used car prices up.

Really, the thing to bear in mind here is that supply was heavily constrained and demand was so much higher than ever before for cars and so all this together eventually washed through into rising prices. So, if you were in a lucky position to have cars to sell you could actually benefit a lot from that situation, but as I said, the number of transactions has come down considerably.

Probably there are two lines that stick out a little bit on this chart, one is the UK price is up almost 30%. By the way, most of this is happening in 2021 and the reason here is that the market is particularly closed off. Not just because of the steering wheel setup on the right side. So, you can’t really import cars into that market which could have helped the supply situation, but also Brexit hasn’t helped and so that’s actually propelled prices in that market to very unhealthy levels and very painful levels if you’re in need of buying a car. For Poland we see the line underneath is also rising quite steeply or well actually quite steadily but to very high levels as well and here the reason is more the economic strength of that country and in particular Eastern Europe is very much focused on used-car markets. They are buying a lot of used cars relative to new vehicles and they are feeling the pain of the supply restrictions. Also, in both markets we recover that a bit later inflation rates are particularly high and this also washes through to car prices and vice versa. The majority of markets between 10% and 15% increased of used– car prices over the past two years and the Nordics have been a bit softer in that in net increase and so that’s what we see in the market at the moment.

Phil: Now, the Omicron variant caused a bit more sort of panic over the winter periods. How strong are our economies and can they weather the Omicron storm, the perceived disruption it may rule?

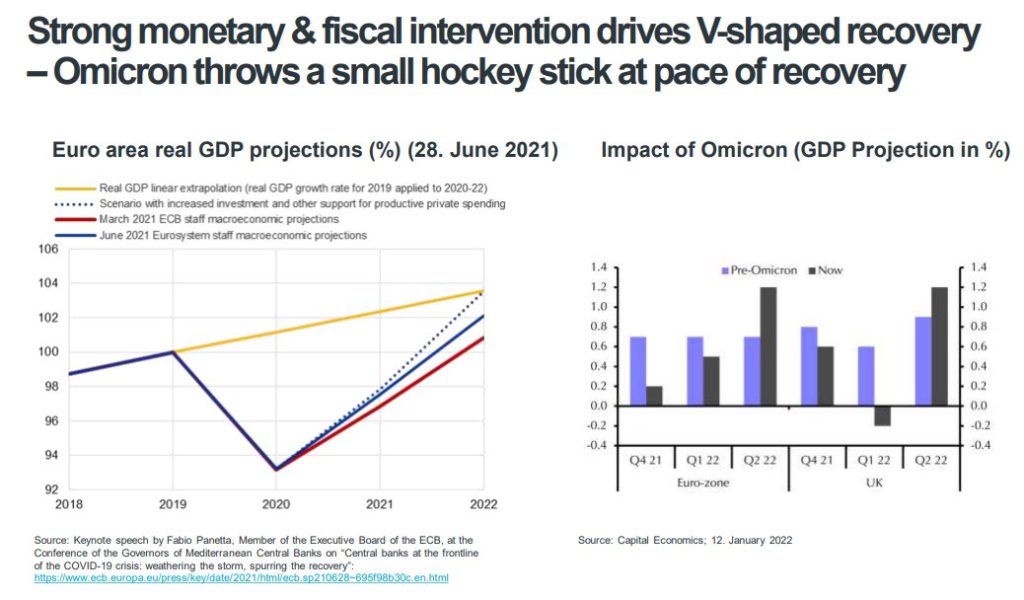

Christof: Yeah, I think what we are seeing in governments and the forecast institute all over the world if you look to the left side we have a pretty fast economic rebound scenario here. When we started in 2020 people were talking about all kinds of different letters to describe the expected recovery scenario. There was a W, there was a U, there was a swoosh, but most of them were pointing towards longer recovery times and then trajectories. Now, what we are seeing really is a V-shaped recovery due to very strong monetary and fiscal intervention, very powerful. You know money was almost free, but actually it was free at times and this was done to really buffer the effects that the crisis; there could have been an economic one, to buffer this off and basically secure that consumer spend was still there and consumer demand was still high in a lot of economies. So, that’s why forecasts have been improving and you see on the left chart how they improve from red to blue. If you were to draw this in 2020 this chart it would have been even more extreme how fast the forecasters had to overrule their previous forecast.

Now, on the right side you see the Omicron effect and what we’ve said on the slide is that Omicron is throwing a bit of a hockey stick into the recovery, but it’s not derailing recovery at all. So, if you look at the dark blue lines they are the Omicron scenario, the one that we’re currently living through and the expectation is basically by the end of next quarter we will have recovered what we have lost in the last quarter of last year and in the first quarter of this year.

Phil: What about inflation? Is there a risk of an overheating we say of economies?

Christof: It’s a good question and one that has been raised most recently as we saw prices for several goods in particular, energy and oil and also goods that are affected by international supply chains rise in prices. So, the price increase is very real. One caveat we have to give is that we’re always comparing and when you see these numbers they’re always comparing the month of the previous year. So, if you look at 2021 December and you compare it with December of 2020 which is around this area here, you can see how inflation was actually negative in those months in or close to zero in some of these markets.

So, obviously if you are comparing now with a let’s say normal month, inflation is higher than it was a year ago, but that’s just one side of the source. So, inflation is actually a risk at the moment but what institutes and banks are seeing and saying and I second that very much is something that can be managed down quite effectively by raising interest rates and we’re seeing this happening in the UK, in the USA. Europe has been underestimating a little bit the inflation that’s what Mrs. Lagarde said and just recently. They haven’t increased rates as of yet, but the expectation is that they might and we have to understand that the interest rates are zero, close to zero or very small levels and that’s certainly not a situation which is good for normal behaviors of prices. So, a slight increase is actually going to be now helpful to keep inflation, to moderate it down. A little bit of a negative effect on stock markets, but the more sustainable scenario than the one that we had two years and three years ago.

Phil: Christof, thank you. We’ll move on now to our next section which is looking at the risk of a bubble build up. Sonja, I come to you. We see a depressed supply of new cars and a rise in EV sales that’s not enough to justify talks about a bubble buildup is it?

Sonja: Thanks Phil and yeah you’re right now and in the near term it certainly is not, but things are expected to look a bit different in the coming years and we just heard about the massive growth of the European EV market and we also heard about all the masking factors and influences shaping our economy and our daily lives at the moment and the question now is whether underneath all of those economic circumstances a remarketing bubble is building up. So, let’s look into the three main risks we have identified and continuously look into.

So, the number one here is with the rise of leasing and private contract purchases, holding periods of new cars decrease and that in turn increases the number of young used vehicles entering the used–car market and here on that graph you see a split between the nearly new ones, so talk about 6-12 months and the up to 36 months typical off-lease cars and we expect the volumes of those to be remarketed. Young used vehicles to rise by more than 50% by 2030 and yes, a bubble could very well be forming out of this.

Phil: We just had a question in Sonja. Is this showing EV only or is it showing all powertrains?

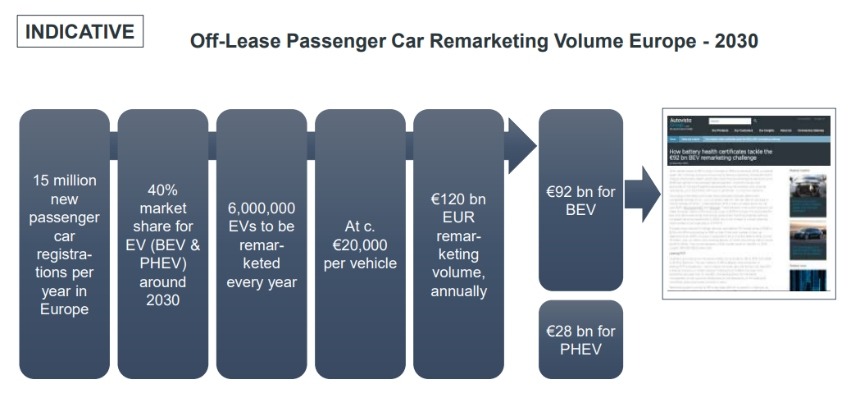

Sonja: This is all powertrains, but we can move on to the next slide and then we’ll see more about EVs in specific because those increasing remarketing volumes they hold true for all powertrains, but here we have a bit of an indication about what we think is happening for EVs.

So, we see remarketing volumes for EVs around 120 billion Euros and that is conservatively estimated on year-on-year. So, annually 120 billion Euros and even very slight changes in car residual values will account for large amounts of money or remarketing risk if you want to say and in this indication one percentage point of residual value roughly equals one billion Euro and with the EV used-car market still not being fully developed infrastructure not yet on a sufficient level in some countries, yes and others not certainly not in all and we have a heavily incentivized new car business. This remarketing risk is very difficult to grasp and requires close observation and risk management.

Phil: So, what exactly is the issue with say battery-electric vehicle remarketing?

Sonja: Yeah, one challenge certainly is the topic of lifecycle depreciation and that will continue to be higher than for a combustion engine vehicles and the main reason for this is the very high pace of technological advancements in BEVs and this example here shows how ranges are developing and over the past two years the average range increased by 100 kilometers or a quarter and that puts really some very realistic price pressure on used BEVs for the near future until ranges are beyond let’s say 500 kilometers.

Not only on the new-car market, but also in the used-car market. So, about three years after we’ve reached that on a new car market and range is just one example. There’s also a charging technology. So, a lot of talk is about the 800 volts charging technology and things like that at the moment. So, this is mainly related to the speed of DC charging and then we also have the capability of upgrading features later in the life cycle and maintaining your BEV more fresh and more up-to-date via features on demand or over-the-air updates and of course another big point and we’ve touched on that before is government incentives and they almost exclusively apply to new-car purchases and thus, they bring down transaction prices and the starting points for residual value positioning and this in combination with the lack of incentives for used car buyers puts a lot of pressure on the willingness to pay basically for used-BEV buyers and that’s probably the main reason why the used-car market for EVs develops more slowly than it does for the new-car market.

Phil: So, what about the internal combustion engine remarketing is after rising values are we going to see them coming down?

Sonja: Yeah, let’s look at that slide where we have the RV development over the past two years split by powertrains and this is an example for France, but it looks very similar in most of the countries and here what you can see is that the different pace of adoption in the used-car market is different and it shows how different BEVs fared versus the ICE and how strong the demand for ICE vehicles is still on the used-car market and yes, we believe that there may be some downward correction in some markets when it comes to ICE.

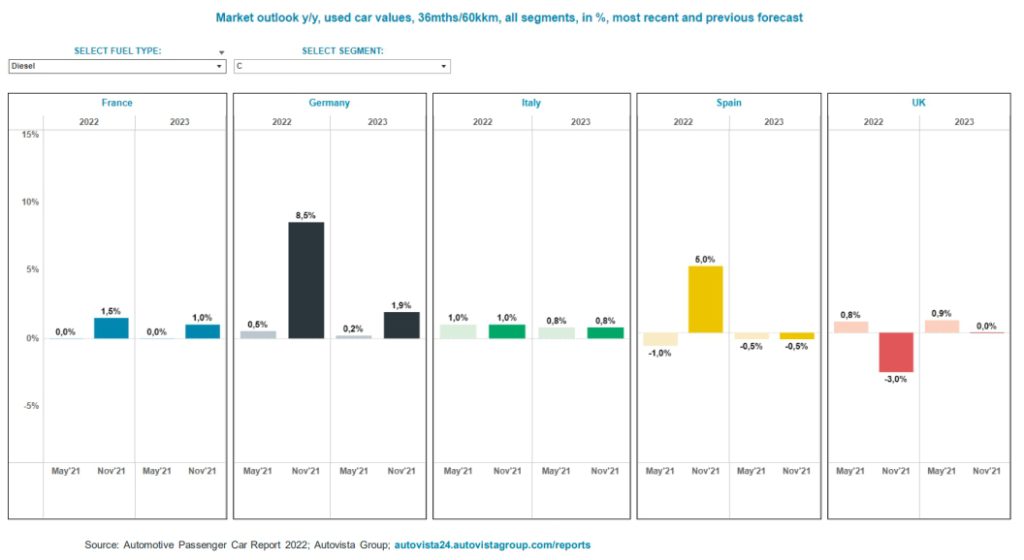

So, for example as we’ve seen earlier in the UK the 30% there will be some downward corrections, but the continued phase out of ICE on the new-car market helps to keep values on used-car markets at a good level. So, yes, there will be some smaller downward corrections but a large share of those RV increases we’ve seen over the past two years will be sustained and in our most recent report we provide very detailed forecasts by market, by segment and by fuel type about what we expect to happen in 2022/23.

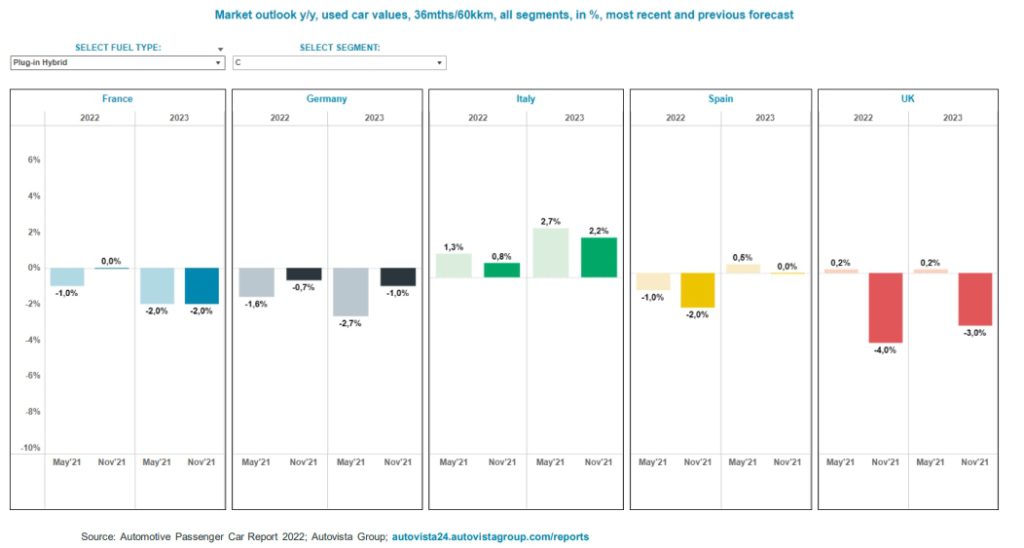

That report is delivered in an online format and includes an interactive multi-country dashboard which illustrates the forecast at a glance and so let’s give a give you a sneak preview into that. As we see here in this very first dashboard we have the forecast for c-segment diesel vehicles which will continue to have rising RVs in all countries, but the UK and even there it’s only a very small correction compared to the 30% increase we saw earlier. If we go to another example from that interactive dashboard we see that for plug-in hybrids in that case the picture is completely different and there will have consistent downward corrections in all countries but Italy and that’s mainly because in Italy the starting point for residual values for plug-in hybrids is comparatively lower than it is for other countries.

So, this report as you said in the beginning was published just now. It’s fresh from the press and you can visit the site that we see on the next slide for as a reminder to find out more and leave your contact details so we can get in touch.

Phil: Indeed, thank you Sonja and I do recommend everybody have a look at this it’s definitely packed full of information, it’s definitely a worthwhile report.

Thank you to all of the panel. We’ll come to the Q&A shortly, but I just want to give a quick summary of some of the points that we’ve discussed in this session. So, the market share of EVs in Europe is almost 20% for the full year 2021 and by 2030 we can expect EV market shares of 50% or more in Europe. There’s several masking factors that keep on disrupting supply and demand balance, but easing expected at least in towards the second half for 2022. Covid19 has propelled prices to new heights. It’s been a run on internal combustion engine cars due to lack of supply and stable demand, but battery-electric vehicle RV is underperformed relative to ICE. Lifestyle affects low levels of used-car market adoption, just some of the reasons for this. ICE RV’s should stay stable in 2022 and 2023 with the exception of the UK market. Electric vehicle RVs will come under pressure in most markets but they will not fall off a cliff.

Now, we have time for a few questions. We’ve had a few coming in already and again, if you haven’t already and you want to there’s a box in the right-hand side of your screen to input your questions. Now, if we don’t get to you during this session we will come to you afterwards. We’ll make contact with you.

There’s a lot of talk about battery health certificates supporting the used-car market, but what impact on value do you think there would be if say a battery was 80% health versus 90% health? Would this matter for different segments and different markets as well?

Christof, you want to pick that one up?

Christof: Yes, absolutely Phil. That’s a good question and one where we have been working together with Twaice and also with Truth and there’s a white paper actually that people can download or a link to that we can also, I hope Phil we can also put in the chat or send afterwards to the participants, or you can Google it. If you Google Autovista24 power of signaling you will find it on the internet.

So, the question was whether it has an impact on residual values whether state of health is 80% or 90% and I mean the key answer is yes and we put some numbers in that white paper as well for you to have a look. There’s one thing that we have to bear in mind, so if we’re talking about 80% where every other particular vehicle of the same model has 90%, then you know there is some sort of mistreatment in place, or bad quality in place and that has an impact. If 80% is a very normal behavior for that particular model, after let’s say eight years of being in the road and 120,000 kilometers or something like that then the 80% still also has an impact but it’s a normal BEV typical depreciation curve.

So, what the battery health certificate is good at if it’s being implemented is to show how first of all different qualities of let’s say manufacturer quality of the battery has an impact and shows in a certificate or how different treatments of the car have an impact and the idea here again have a look at the white paper, it’s quite detailed if we want to establish a win-win situation here, that if people treat their battery better, so not charging to more than 90%, not too much fast charging then this should wash through in a much better battery quality and that should show in remarketing results and there’s a win-win for everyone. So, we’re not trying to punish anyone here, but really a win-win scenario for everyone.

Phil: Indeed, and I have got that link. I’m just going to put it into the chat box there so if anyone’s interested in reading that white paper the details are in the chat box on the right-hand side of your screen.

In 2021 Tesla delivered 900,000 cars. It seems that Tesla wasn’t affected by the semiconductor, the microchip crisis. Is that your point of view and do you think that Tesla will now be disrupted by other OEMs in the future as they come onto the market?

Roland, do you want to pick that one up?

Roland: I think Tesla paid more for chips in 2021 and 2020 than in the years before. There was a lack of chips on the markets. The advantage of Tesla was that they could make it to oversimplify, to buy whatever chip they wanted and reprogram it or reprogram the car around it. Tesla’s vehicles are more soft wired than hardwired, so they had it easier.

For their future prospects, whether they can maintain the lead in the market? Yes, for a considerable time. We know they are supply constrained, we know they have much more demand than they can deliver. Very long delivery times, logistic challenges present only in two or three segments. So, they’re not covering for instance their home markets, the United States in all states, they are still banned from establishing distribution centers in 20 of the US states. So, there’s a lot of untapped potential for Tesla in the market considering the narrow portfolio they have today and considering the logistics and market representation which they can improve.

Phil: Thank you and we’ve had a couple of questions come in. Some people have had to unfortunately drop out and come back into the presentation, so just to reiterate again the webinar slide and the video, this presentation will be available after this session has ended. So, if you’ve missed anything don’t worry, you will have the opportunity to catch up.

Do you see risks for new BEVs like the Volkswagen id3 that has a range below 500 kilometers?

Should we go with that one Sonja?

Sonja: Yeah, I think it may be linked to what I said earlier about the 500 kilometers of range being available on the used-car market as well and that’s a point where people stop worrying about range altogether, but that in turn doesn’t really mean that there is a bigger risk for cars that don’t have those 500 kilometers right now. You always have to compare with what is available, what you need for your use case and of course you always have the versions with different battery packs available.

So, no there’s not party fault a risk for all cars that don’t have those 500 kilometers, but of course once they get older and enter the used-car market they will be in a stark competition with newer models that are maybe available with higher ranges at lower costs because those technological advancements have a very high speed at the moment. So, yes they will be in a competition and they will have to take that competition, but that doesn’t automatically mean that they are all under a huge risk. It just means that once we’re over 500 kilometers people just don’t worry about that topic anymore and other things get much more important like the speed of charging.

Christof: Maybe if I could just add a little bit on. I mean what Sonja has described in terms of range progression washes through into life cycle depreciation. So, it would be a risk if now suddenly cars come to market which have 700/800 kilometers of range in that WATP setup and cost the same. So, that would be a huge risk of course, but that’s not something that is likely to happen anytime soon. Everything else is currently already happening right? So, every year range goes up and as long as we are under that sweet spot of beyond 500 real range, life cycle depreciation kicks in but that is already baked into the forecast and into the market. So, it’s not a new risk, it’s a BEV life cycle appreciation fact. We have a lot of data and we can observe that in a lot of models.

Phil: Excellent, thank you.

We are coming to the end of our time. So, we’ll leave the Q&A there, but thank you for everybody who has submitted a question. As I said, we’re not going to ignore them, we’re going to pass them on to our panel afterwards and we’ll be in touch to give you an answer there and again, if you have any questions, if you’ll be watching this or you think of something a little later on today the contact details of our panel are there on screen. So, please do get in touch if you’ve got any thoughts, you want to know any more information and again don’t forget to look at the automotive trend report 2022 and register your interest. The link to our landing page is there on screen and again it will be available in the catch up and the on-demand as well so don’t worry about noting that down and it covers a vast array of information across different segments looking at electric across new-and used-vehicles markets as well. So, again I’d like to thank our panel for joining me. It’s been a very interesting discussion today and don’t forget as well to check out autovista24.com for the latest news, features and data analysis of the automotive market and while you’re there don’t forget to sign up to our daily email where amongst other things you’ll get notifications of future webinars that we’re planning to hold. Thank you all very much for joining us and we’ll see you soon.